The pandemic has proven to be a powerful source of motivation for the housing market. After grinding to a halt in March and April like the rest of the economy, home sales and prices have bounced back with a vengeance.

Several monthly housing-related reports were released this week and they all sang a similar tune. Economists have been warning that the good times won’t keep rolling at the same pace for very long. They view the current housing market strength partly as a correction or a clearing of the backlog of pent-up demand created during tighter lockdown months.

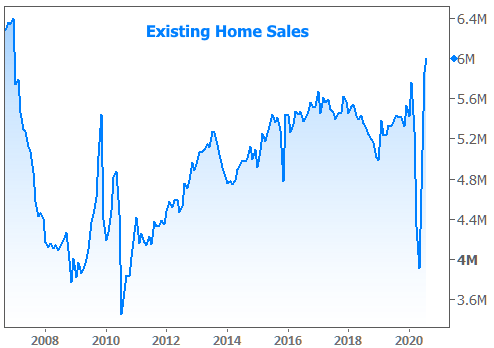

Sure enough, after increasing by roughly 20% in each of the previous 2 months, sales of existing homes improved by less than 3% in August. But before you read too much negativity into that, consider that the modest gain improves on the best levels in nearly 14 years. Alternatively, forget the pace of growth and simply consider how it all looks on a chart.

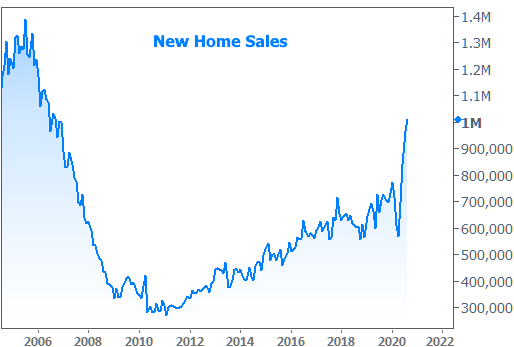

Incidentally, Existing Home Sales–while still accounting for a much higher number of homes sold–are drastically underperforming New Home Sales in terms of growth. If we didn’t have the chart above telling us that existing homes are indeed selling like hotcakes, we might conclude new homes are winning because they’re the only game in town.

While it is true that builders have been more capable of bringing inventory to the market than existing home sellers post-covid (and possibly that some buyers are more comfortable shopping for new homes), there is an even bigger factor to consider. Demand is extreme for homes in the suburbs, and that’s where builders do most of their building. A simple equation with a simple result:

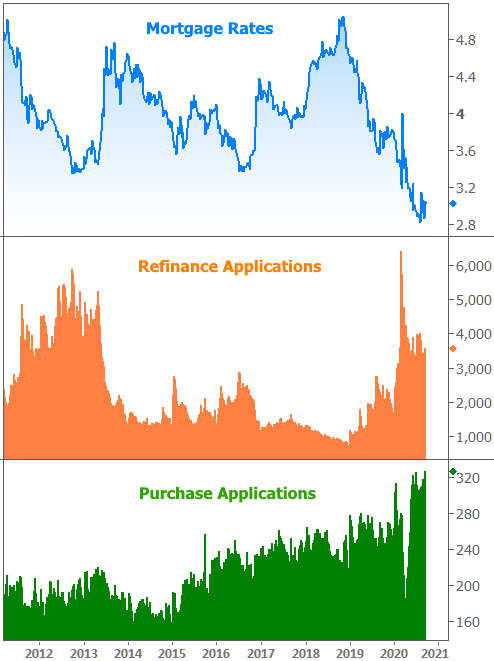

Moving on from home sales to home loans, sleep and free time are foreign concepts for most mortgage pros at the moment. Lenders are pushing the limits of capacity. Everything you’ve heard about mortgage lenders being busy and turn times being long is not only entirely justified, but possibly a vast understatement. We’ve seen crazy times, but never anything quite like this.

Considering the operational hurdles presented by the pandemic, and the chaos created by the unexpected refinance fee, the level of mortgage applications being processed each week is nothing short of impressive.

Wait, what’s this about a refinance fee?

Fannie Mae and Freddie Mac are the two government sponsored agencies that guarantee timely payment of principal and interest to the investors who front the money that finances the American mortgage market. This guarantee means that more investors are willing to participate, and at more advantageous rates for homeowners. Naturally, not every mortgage is repaid perfectly. Sometimes, payments are missed. In more serious situations, loans can end in foreclosure, short sales, etc. In those cases, the housing agencies are there to act as a backstop ensuring investors are made whole.

In order to foot that bill, Fannie and Freddie collect fees on loans that they guarantee. Shockingly, these are called guarantee fees (or guaranty fees” with a “Y” in the case of Fannie Mae). The mortgage industry and the rest of this article will typically refer to them as G-fees.

There are g-fees you see and those you don’t. If you are quoted a higher rate because you have a lower credit score, higher loan to value, or are buying an investment property, your loan is mathematically riskier. The agencies will require more money from your lender to guarantee your loan so your lender either charges you more upfront or simply a higher rate. Either way, this is the most obvious way that the g-fee comes into play. But even if you’re a perfect borrower with an 800 credit score putting 40% down on an owner occupied home, the agencies are still going to collect a g-fee. You just won’t see it because it will come off the top of every interest payment each month.

G-fees have risen and fallen over the years (mostly risen), and that’s been especially true after the financial crisis. The average g-fee on Fannie/Freddie’s entire portfolio comes out to just under 50 basis points (or 0.5% of the loan amount).

It was a rather jarring revelation, then, when the agencies announced ANOTHER 50 basis point g-fee to be imposed on all refinances back on August 12th. The fee was to apply to any loan delivered to the agencies on or after September 1st. “Delivery” is a fancy term for the agencies giving a loan their stamp of approval–aka “guaranteeing it.”

It can take several weeks for that to happen AFTER the loan is closed. As such, the initial August 12th announcement with a delivery deadline of September 1st meant that lenders would have paid the new fee out of pocket for hundreds of billions of dollars of loans.

That’s why rates spiked so quickly in early August and why they recovered several weeks later when the deadline was pushed back to Dec 1.

It’s unfortunate that the press surrounding the fee has only the Dec 1st date to rely on. It would be a better service to consumers if the agencies could have specified a date that the loan needs to close by. Dec 1st seemed like a long way off back in late August. But when we account for the 2-5 weeks of lead time to get a loan from the closing table to “delivery,” it’s a different story.

In fact, many lenders have already re-implemented the fee. They figure, depending on the lender, it will take 30-60 days for a loan to close and another 15-45 to get the loan guaranteed by the agencies. That gives us a total time range of 45-105 days, and December 1st is right in the middle of that range.

For some lenders, rates recently spiked significantly in a single day as they reimplemented the fee. For other lenders, it’s only a matter of time. In terms of nuts and bolts, the fee raises rates by 0.125-0.25%. Alternatively, it can be paid upfront as 0.5% of the loan amount.

Either way, the important point is that the fee will soon be back for every lender (if it isn’t already), and in a bond market that has been exceptionally flat, it’s the single biggest consideration for mortgage rate movement right now.