Rising rate headlines are nothing new, but there was a bit of a double whammy this week… or triple, depending on your point of view.

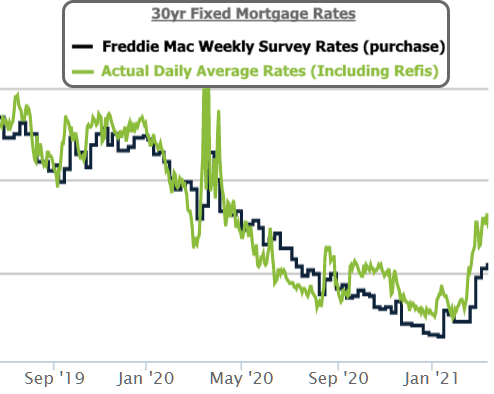

Whammy 1: Highest Rates in a Year

It’s March 2021, and you’d now have to go back to March 2020 to see higher mortgage rates. It will take mainstream media a while to get caught up with this new reality because the most widely cited mortgage rate survey tends to lag behind sharp moves like this.

Whammy 2: It’s Been a Bumpy Ride

And that brings us to “whammy 2.” This move has been surprisingly abrupt. Not only have rates risen about as fast as they ever do over the past 2 months, there have also been several false starts where it looked like rates were catching a break only to jump much higher in a single day.

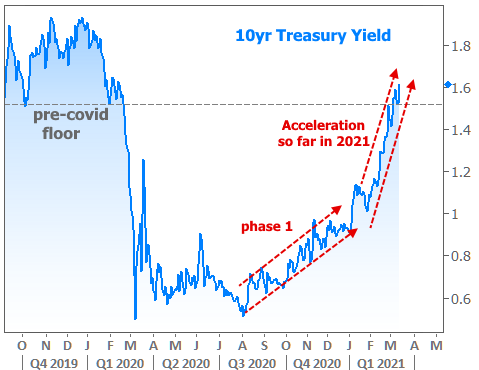

Friday was one of those days. The first 4 days of the week were among the more hopeful and resilient we’ve seen in 2021. 10yr Treasury yields (a benchmark for momentum in longer-term rates like mortgages) were holding safely below their recent 1.62% ceiling, even trading below 1.50% briefly on Thursday.

Things changed abruptly on Friday. A stark absence of any overt, short-term motivation makes this whammy all the more frustrating. In other words, there weren’t any big, new developments that caused the jump. It was just the way traders traded.

The chart above may not look like much, but it’s just a small section of a bigger trend. And that bigger trend represents a noticeable acceleration from the previous trend of rising rates. Incidentally, this week’s installment takes 10yr yields back above their pre-covid floor for the first time.

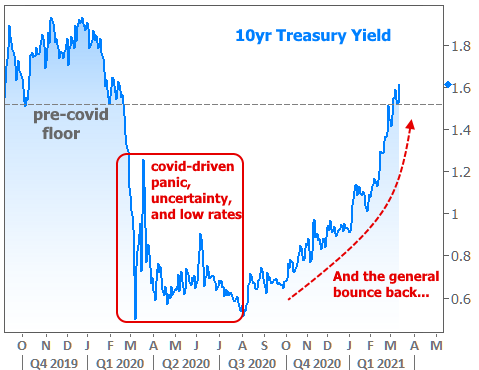

Speaking of covid, that’s ultimately why traders are trading this way! The acceleration in 2021 is all about increased vaccine distribution, sharp declines in case counts, and the passage of more covid-relief stimulus (which hurts rates in two ways: by increasing economic activity/inflation and by adding Treasury supply). Here’s another look at the same chart, this time with emphasis on the “covid effect” and the subsequent bounce back.

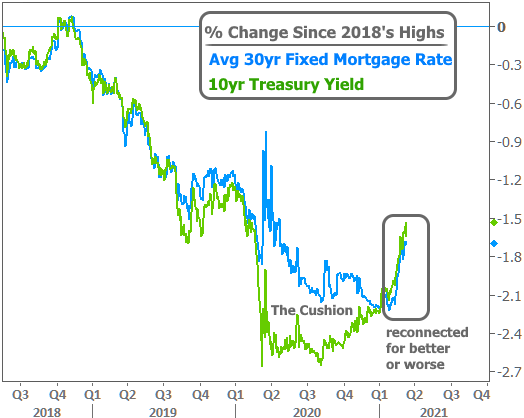

If it doesn’t feel like mortgage rates got quite as much warning as suggested by the Treasury charts, that’s because they didn’t! To be fair, we did warn against complacency when rates were still at all time lows, but it’s one thing for a newsletter to point out the risks and quite another to see rates jump half a percent in February alone.

Why did rates wait to “get the memo” from Treasuries? In a nutshell, the mortgage market couldn’t keep pace with the broader bond market. Mortgage rates were able to keep falling and remain lower because they were still getting caught up to the move in bonds. We’ve referenced this several times as “the cushion” and here’s yet another look.

Whammy 3: Additional Costs For Investment Properties and 2nd Homes

The first 2 whammies are bad enough (or good enough, if you’re willing to view higher rates as the logical byproduct of the fight back against covid). The third thankfully only applies to a small section of the mortgage market, but for those with 2nd homes or investment properties, it may sting a bit.

In the final days of the previous administration, Treasury and the FHFA amended the terms of Fannie and Freddie’s bailout agreement in such a way as to limit the amount of certain types of loans that could be acquired. This week, Fannie Mae finally formalized the announcement and began contacting lenders that had too many 2nd/Investment loans on their books.

The result? Several lenders immediately jacked up rates/fees on these loans–some by huge amounts (like 5+ points, or $20k on a $400k loan). Those who didn’t respond immediately are expected to follow suit in the near future, even if not all of them will be as severe as the early adopters.

What does this mean for you? Simply put, if you have an un-locked investment property or 2nd home loan that’s in process, it may have just gotten a lot more expensive. That won’t be the case for everyone though (not at first, anyway), so definitely check with your mortgage professional to see what your options are.