Low-interest rates have been one of 2020’s most pleasant surprises. Heading into the end of 2019, there were more than a few reasons to worry that rates would be moving steadily higher this year. The upside is that they would at least be starting that journey near enough to all time lows and that the same forces pushing rates higher would also help stocks pursue new all-time highs.

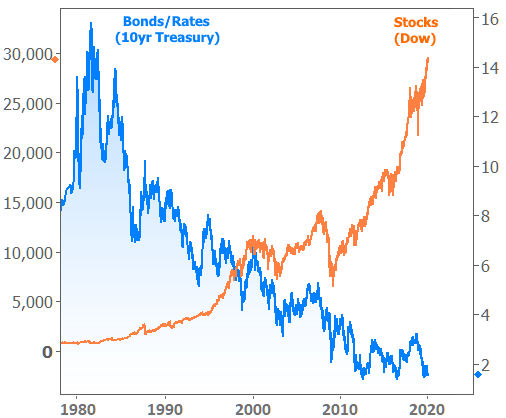

But wait… How can we be talking about rates near all-time lows while stocks are near all-time highs? Doesn’t conventional wisdom dictate that rates and stock prices typically move in the same direction?

Yes and no. It is true that economic strength generally puts upward pressure on both stocks and rates (and vice versa), but that’s far from the only factor. Inflation has historically been a fairly critical factor for rates and it really threw the long-term relationship with stocks out of whack in the early 80’s. Hyper-inflation set the highest bar we’re ever likely to see for rates, and most of the past 40 years has simply been a return to earth. Meanwhile, stocks have done what stocks generally do.

While there will always be “down times” for stocks, in the long run, they’ll continue to grow as long as the economy grows. Rates, on the other hand, are designed to oscillate inside a range (even though the 80’s make it seem otherwise) regardless of the size of the economy.

Unless the economy is actively moving into or out of a recession, our best chance to actually see correlation between stocks and bonds is to look at much shorter time-frames. Odds improve when the overall market is in the middle of reacting to some temporary, unexpected shock. The Fed complicates things as accommodative Fed policy generally acts to push stocks and bond yields in opposite directions.

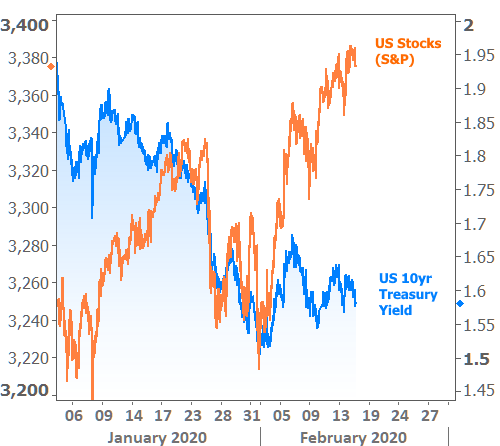

Right now, we do indeed have a friendly Fed and we’re definitely not actively moving into or out of a recession. In other words, there’s very little to inform stock/bond correlation apart from unexpected market shocks like coronavirus. As the following chart shows, coronavirus took a clear toll on both stocks and bonds in late January. The improved outlook in early February prompted a rebound, but bonds haven’t been as quick to move back up.

Even without coronavirus, the general trend over the past year has been toward higher stocks and lower rates. Correlations certainly emerged when the trade war hit (that’s one of those “unexpected shocks”), then again when trade prospects improved, and most recently amid the coronavirus volatility. But in the bigger picture, we’re still left with bonds resisting a move higher despite stocks surging to all-time highs.

To reiterate, the Fed is a big piece of that puzzle. They’ve been able to offer the market accommodation in a few ways recently. The most significant way is simply their guidance about what it would take for them to hike rates. Strong economic data would normally cause concern for Fed rate hikes, but that won’t do it this time around. They’d have to see a big uptick in inflation, and that’s proven to be elusive time and again in recent years (so much so that policy officials openly express confusion as to why it hasn’t shown up). Additionally, the Fed repeatedly says the next economic downturn will see a reprisal of the same sort of bond buying programs that juiced financial markets during the great recovery (2011-2015).

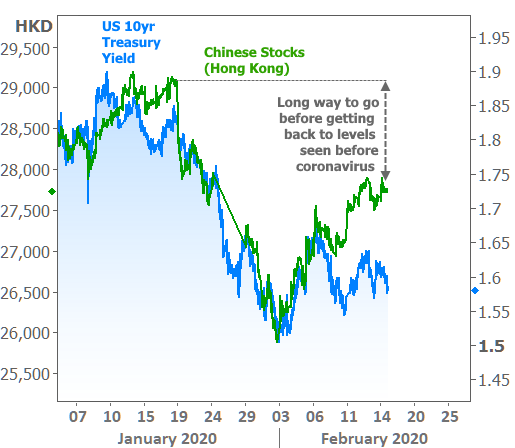

All that to say, bonds/rates have some reasons to avoid a quick return to recent highs, even as the stock market can justify it. Coronavirus adds to the discrepancy because bonds are accounting for the economic impact likely to be seen in the near future while stocks are fresh off a strong earnings season and generally riding the wave of ongoing US economic expansion. Bonds are also a global safe haven in times of uncertainty. The US economy is decent for now, so US stocks are forgiven for being as high as they are. But the Chinese economy will undoubtedly take a bigger hit from coronavirus–so much so that investors haven’t been nearly as quick to fuel a rebound in Chinese stocks.

Bottom lines on stock/bond discrepancy:

- A friendly Fed serves as a backdrop for generally lower rates and higher stock prices

- Coronavirus hurts the Chinese and global economies more than the US economy

- Global investors use the US bond market as a safe haven (which puts downward pressure on rates)

- The US bond market always does more to price in economic expectations for the future than the stock market