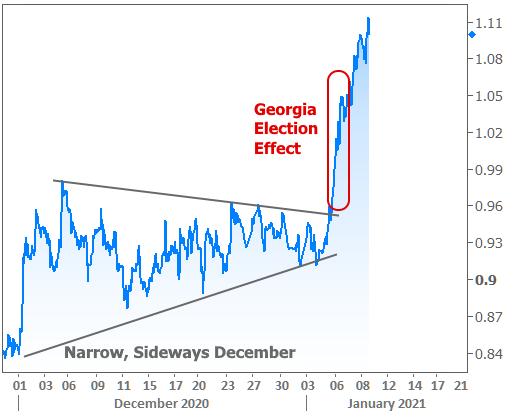

While it might not seem like the sort of thing mortgage rates should care about, the senate run-off election in Georgia was by far and away this week’s most important event. This wasn’t a surprise either. In fact, interest rates have been bracing for this potential impact since the inconclusive results in early November. But why do rates care about politics?

Actually, they don’t! Not too much, anyway. Rates care about the prices and yields of certain bonds in the bond market above all else. Bond prices can take a variety of cues, but the most basic and most objective input is that of supply and demand.

Supply and demand can be influenced by several underlying factors. For instance, the Fed currently buys more than $100 billion in bonds each month. That has a huge impact on the demand side of the equation. Higher demand=higher prices=lower rates (bond price varies inversely to rates).

The most relevant example of the supply side of the equation in 2020 has been that of fiscal stimulus. If higher demand is good for rates, then higher supply is bad–all other things being equal. With that in mind, the paradoxical rate spike in March 2020 makes more sense. After all, $2 trillion of covid-relief stimulus required a massive amount of new US Treasuries. Mortgage rates take their most direct cues from mortgage-backed bonds which, in turn, take substantial cues from Treasuries.

For all these same reasons, when the prospect of another round of stimulus became more of a reality on December 1st, Treasury yields spiked immediately. This was a smaller round of stimulus versus March 2020. You’ve likely heard as much as you care to hear about $600 vs $2000 direct payments. Had there been 51 votes in the senate for a bigger stimulus bill, rates would have jumped more abruptly.

That brings us full circle to the GA senate election. In 2 weeks, there will be 51 democratic votes in the senate (counting Harris as a tie-breaking vote). While a few moderate democrats have already said they wouldn’t support $2k direct relief payments, the additional 2 seats mean that some measure of increased stimulus is now likely. And to reiterate, more stimulus = more Treasury issuance = upward pressure on rates.

Beyond that, there’s also the general truth that it’s easier for the government to pass bills that incur Treasury issuance when one part has control of the House, Senate, and the White House. To be clear, this isn’t about democrats or republicans. It’s about the absence of political gridlock. In any event, the charts don’t lie.

So what’s the damage for mortgage rates? That really depends on your perspective. In the bigger picture, rates are still amazing, and they haven’t moved much higher at all yet. It didn’t hurt that we’d just hit another patch of new all-time lows a few days prior. But since the GA election, the average 30yr fixed rate is up at least an eighth of a point 0.125%. Any headlines you may have seen this week regarding “all-time lows” (even if they were published on Thursday) are now stale and outdated.

The headlines in question rely on Freddie Mac’s weekly rate survey which comes out every Thursday. While there’s nothing wrong with that data for broad tracking purposes, it simply cannot be relied on for day-to-day changes. That’s especially true when there are big swings on Wed-Fri (Freddie’s data heavily favors Monday’s rates and it doesn’t even count Thu/Fri). In other words, yes, rates arguably were at all-time lows on Monday. By the time Freddie reported that on Thursday, rates were sharply higher.

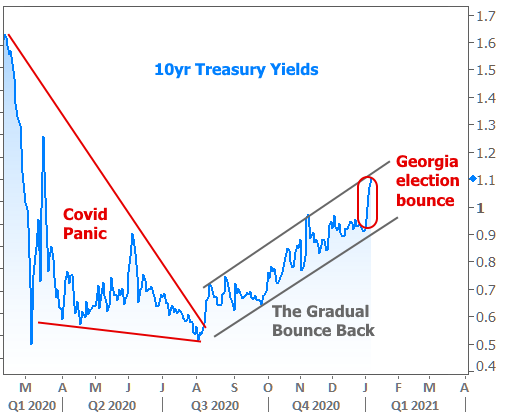

Let’s forget about what’s already happened and talk about what might happen in the future. The big question is whether or not we just confirmed an ongoing trend toward higher rates. As far as Treasuries are concerned, that’s certainly a risk. Note that the Georgia election bounce keeps the rising yield trend intact.

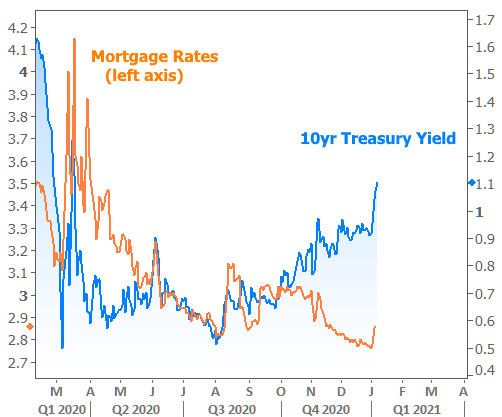

But when we add mortgage rates to that chart, the implication is less clear.

One might even conclude that mortgage rates don’t care that the broader bond market is pointing toward higher and higher rates. That would be a mistake though, for the reasons laid out in great detail in the last newsletter (definitely read that if you missed it). In other words, we need to pay more attention to the threat of rising Treasury yields now (as this week’s mortgage rate spike confirms).

The good news there is that the case is not yet closed on 2021 being the year of rising rates. Granted, that is the higher probability scenario, but it doesn’t necessarily need to look like 2013 or 2018. Those sorts of rate spikes require a key ingredient that is only looming on the horizon at an uncertain distance: a decrease in accommodation from the Fed.

In 2013 it was the “taper tantrum” when the Fed announced it would gradually decrease its bond buying. In 2018, it was a relentless series of rate hikes despite signs of a global economic slowdown and still-tame inflation. This time around, the Fed says it’s determined to treat the post-covid economic expansion with more care, but there’s no getting around the fact that rates are going to react as soon as the Fed announces a bond-buying change.

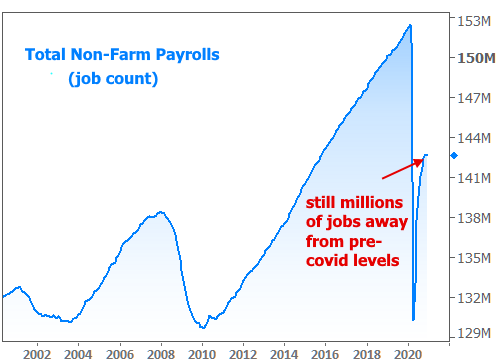

For that to happen, inflation will need to be much higher than it is today, and millions upon millions of people will need to be back at work. This week’s most recent installment of labor market data shows just how far we have left to go.

That sort of economic progress is highly unpredictable in general, but even more so in the age of covid. Much depends on the vaccine roll-out and the realization of any permanent changes to the labor market that some economists have suggested (i.e. how many companies will realize that they don’t need as many employees as before based on lessons learned during the pandemic? How many sectors will endure permanent change due to post-covid consumer behavior?)

What kind of time frame are we talking about here? Fed members generally don’t see a hike to the Fed Funds rate until 2023-2024. But it’s not the Fed Funds Rate that matters. It’s the asset purchases (which include the MBS that drive mortgage rates).

The Fed has left things very open-ended when it comes to the line in the sand that signifies it’s time for a change. The same was the case in 2013. This time around, however, they will likely telegraph the decision much more carefully.

What will they be looking for in general? It all comes down to jobs and inflation. Unemployment is still roughly double what it was before covid. If we can close most of that gap, and if inflation is holding at 2.5% or higher, or if it even looks like we’re well on our way toward those goals, expect rates to be well on their way to pre-covid levels.