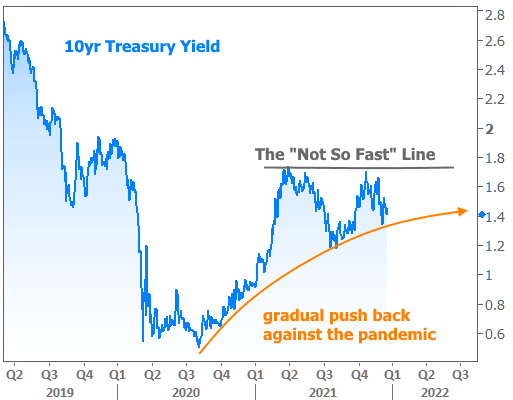

Sure, we could write a headline that attempts to distill the concept of a big picture struggle between the forces exerting upward pressure on rates and those stepping in to push back in the other direction. Or we could just introduce the “not so fast” line, and let a chart do the talking.

Lines like these are over-generalizations to some extent, but as long as we understand that there are multiple factors in play each time rates bounce on the floor or ceiling, it doesn’t matter. All we’re really trying to do is visualize the gradual recovery from the pandemic and the setbacks that have pushed rates back in the other direction.

Thinking about the more recent past, rates have been reluctant to move below the orange line due to things like higher inflation and tougher central bank policies. General progress against the pandemic was more relevant to the orange line in Oct/Nov, but the emergence of Omicron means the pandemic is once again putting downward pressure on rates.

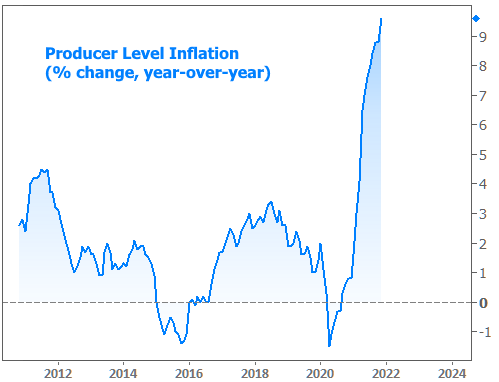

All of the above showed up in charts at various points this week. Yields (aka “rates”) surged lower to start the week as the weekend’s omicron news stirred up concerns about economic impacts and risk aversion in financial markets. Another inflation report showed the highest levels in decades. The Fed and other central banks made policy updates that caused brief upward pressure for rates before pandemic-related news said “not so fast” by the end of the week.

In the chart above, “Fed” refers to the scheduled policy announcement from the Federal Reserve. The Fed announced that it would be decreasing its monthly bond purchases at an even faster pace. While this wasn’t unexpected, it was unprecedented. There was also some uncertainty about how big the change would be, and the Fed chose the faster option (i.e. less friendly for interest rates).

Rounding out Wednesday’s bad news for rates, updated Fed forecasts showed a big shift in the outlook for rate hikes with the median view of the Fed Funds Rate now at 0.75-1.0% by end of 2022, up from 0.0-0.25% last time. Here too, the results were not unexpected, but the shift toward a higher rate mentality was surprisingly unanimous compared to previous forecasts.

One day later, the Bank of England unexpectedly hiked its policy rate. Most market participants expected them to wait for the next meeting due to surging covid numbers in the UK. The European Central Bank (ECB) didn’t rock the boat much, but the net effect was still negative for bonds/rates.

Despite the headwinds from central banks, rates spent most of the day on Friday at the lowest levels of the week. At first glance, this is an impressive level of resilience for the bond market, but it’s probably best viewed as a sign of the times. The week’s stock market gyrations tell the same story. Stocks fell early and late in the week with covid-related headlines being the most prevalent explanation.

In the bigger picture, the important thing to understand about the “not so fast” line is that it represents one side of a consolidation pattern. It presents a case for fear and caution while the orange recovery line makes the opposite case. Rates won’t remain stuck in the middle forever. As tired as we all may be about deferring to the same old scapegoat, the direction of the breakout will most likely be informed by how things go with the pandemic.

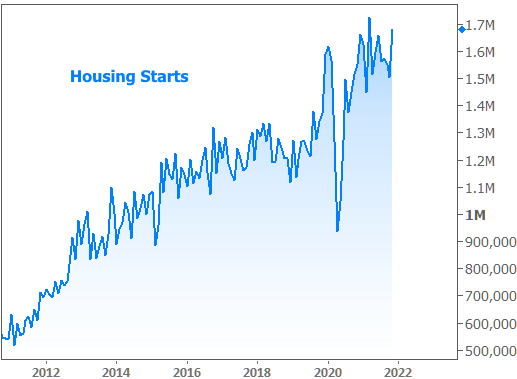

In other less consequential (but still potentially interesting) news/data from this week, new housing construction increased by 11.8% in November. The total number of “housing starts” was very close to long-term highs.

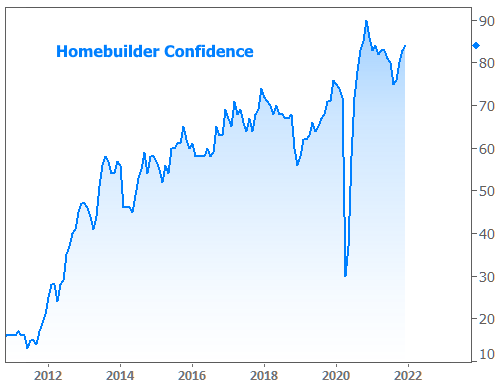

Unsurprisingly then, builder confidence also remained in good shape, per the NAHB’s Housing Market Index.

Next week is fairly slow and much-abbreviated due to the Christmas holiday. Markets will be closed all day on 12/24 and open for only a half day on 12/23. The following week is notorious for light participation and a high variety of trading motivations in financial markets. As such, we won’t get a clean look at underlying market momentum until early January.